The Qantas Group delivered strong earnings in FY24 while investing in customers, new aircraft, benefits for employees and returns for shareholders.

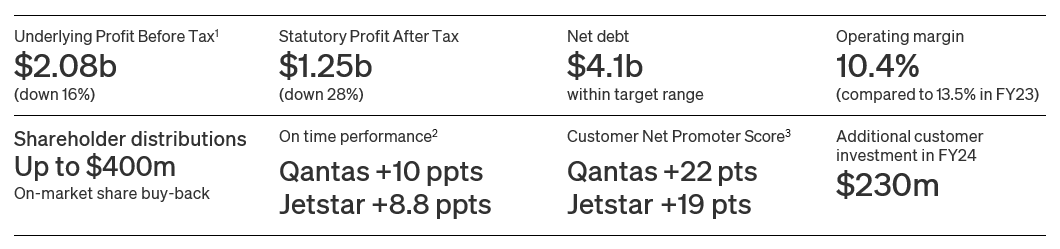

The Group achieved an Underlying Profit Before Tax of $2.08 billion and a Statutory Profit After Tax of $1.25 billion for the year ending 30 June 2024.

Overall earnings reduced compared to last year as fares moderated with the return of market capacity, spending on customer initiatives increased and freight revenue reduced predominantly in the first half. Group Domestic unit revenue provided positive momentum in the second half, increasing on 2H23 levels.

Qantas and Jetstar saw significant improvements in operational performance and customer satisfaction across the year, driven by investments in its operations, enhanced food and beverage, an overhaul of Qantas’ digital platforms and increased availability of frequent flyer seats.

The Group’s fleet renewal continued with 11 new aircraft arriving during the year, including five Jetstar Airbus A321neo Long Range aircraft and two QantasLink A220s, as capital expenditure increased to $3.1 billion. The new fleet provide improvements in operating cost, network flexibility, passenger comfort and emissions.

As part of recognising the efforts of its people, 23,000 non-executive employees will receive a $500 staff travel voucher to go towards already heavily discounted standby fares. This is in addition to a $500 voucher provided to employees in February, bringing the total to $1,000 for the year.

Looking forward, bookings and travel demand remain stable with intention to travel and revenue intake trends remaining positive across all flying brands.

Comments from Qantas Group CEO Vanessa Hudson

“This result shows the underlying strength of the Group’s integrated portfolio. Qantas benefited from increased corporate and resources travel and ongoing high demand for international premium seats while Jetstar delivered its highest result as it grew to meet increased demand from price-sensitive leisure travellers and saw the benefits from its new aircraft.

“The introduction of Classic Plus, with millions of frequent flyer seats, helped drive member engagement and strong earnings for Qantas Loyalty.

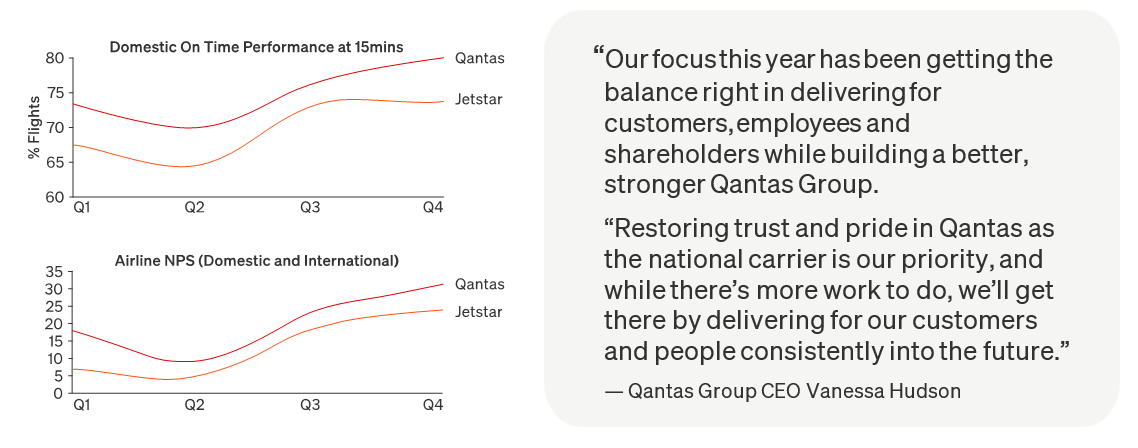

“The investment in operational reliability and customer initiatives delivered a positive improvement in on time performance and customer satisfaction with Qantas ending the year as the most on time major domestic airline.

“Our strong financial performance and balance sheet will allow us to continue to invest in our largest ever fleet renewal program, which will benefit our customers and people, as well as delivering shareholder returns.

“These investments come at a time when Australians are continuing to prioritise travel over other spending categories, with intention to travel over the next 12 months remaining high.

“I want to thank every one of our people for the professionalism, hard work and commitment to delivering for our customers.”

Group Domestic

Group Domestic delivered $1,361 million in Underlying earnings with an EBIT margin of 14 per cent, supported by Qantas and Jetstar’s dual brand strategy.

Jetstar grew its domestic network by 15 per cent year on year as demand for low fares travel strengthened, while Qantas’ capacity increased by 1 per cent as the continued return of corporate and small business travel more than offset a softening of demand for domestic premium leisure travel.

Growth in resources sector flying continued with charter revenue up 18 per cent on the previous year, with the Group adding three mid-life A319 aircraft to service these customers during the year.

Qantas’ on-time performance was particularly strong in the fourth quarter nearing long term averages with 80 per cent of flights departing on time, while 74 per cent of Jetstar flights departed on time. This improvement helped drive customer satisfaction with Qantas Domestic’s Net Promoter Score increasing by 24 points[4].

Qantas’ mishandled baggage reduced by almost a third year on year and is now better than pre-COVID levels.

The Group also provided more than 45,000 Bonza and Rex customers with free of charge flights after they ceased operations.

Group International and Freight

Group International earnings moderated to $755 million Underlying EBIT as the return of global airline capacity put downward pressure on fares and freight yields declined.

The Qantas Group returned to pre-COVID international capacity in May 2024[5], with the return of more aircraft, including two more A380s. The revenue from this additional flying was offset by an anticipated increase in competitor capacity, which resulted in an 11 per cent reduction in unit revenue, although the decline slowed in the second half.

The performance and popularity of Perth-London, Perth-Rome and since July, Perth-Paris, continue to provide confidence in the launch of non-stop flights to London and New York from Melbourne or Sydney, with the A350- 1000ULR expected to arrive in mid-2026.

Jetstar’s international network[6] saw significant growth and an 11 per cent margin for the year. Some of the new A321LR aircraft have been used to grow short haul international routes to destinations like Fiji and Bali, allowing for B787s to be redeployed on long haul routes such as east coast Australia to Japan and South Korea.

Qantas Freight recovered in the second half of FY24 after a challenging first half, with a continuation of the fleet simplification program introducing two A330 and three A321 freighters this year. International freight yields moderated faster than expected but continue to hold more than 150 per cent above pre-COVID levels.

Qantas Loyalty

Qantas Loyalty continued to perform strongly in FY24 with a record Underlying EBIT of $511 million as it delivered major program improvements for members.

A record number of points were earned and redeemed across the year, including a record number of reward seats booked, and there was a 14 per cent increase in the number of active members compared to the previous year.

The introduction of a new flight redemption product, Classic Plus Flight Rewards, was one of the biggest expansions of the Qantas Frequent Flyer program in its history, unlocking more redemption opportunities to drive program engagement. Classic Plus was launched on international flights in April 2024 and once rolled out on the Qantas domestic network by the end of calendar year 2024, members will have had access to more than 20 million reward seats.

Qantas Loyalty continued its expansion into holiday packages by purchasing the remaining stake in online travel business TripADeal. The acquisition will drive value in the Group by combining Qantas and Jetstar’s extensive network with the growing curated tour market, as well as benefitting members. The total transaction value of TripADeal bookings has increased four-fold since 2022.

The program continues to see growth in white-label insurance and home loan products and reached more than 800 coalition partners including major new partnerships with Ticketek and Accent Group.

Financial framework and shareholder returns

The Group’s Financial Framework recognises the importance of investing in our business and people to deliver positive customer, social and environmental outcomes to drive sustainable shareholder returns.

The Group ended the year with $10.2 billion of liquidity, including $1.7 billion in cash, $1 billion in undrawn facilities and $7.5 billion in unencumbered assets.

Net debt rose to $4.1 billion at the end of June 2024 as new aircraft were delivered, $869 million of share buy-backs were undertaken and bonuses were paid to around 20,000 employees. Net debt is now in the bottom half of the target range ($3.9 – $4.9 billion).

The strength in the balance sheet, combined with increased cashflows, is expected to underpin future aircraft deliveries and shareholder returns.

The Group will distribute up to $400 million to shareholders in the first half of FY25 through an on-market share buy-back.

Fleet

The Group is seeing the benefits of the biggest fleet renewal program in its history, with 11 new aircraft arriving over the past year. This will increase again, with 20 new aircraft due to arrive in the coming year, and the return of the remaining two A380s over the next 18 months.

Fifteen Jetstar A321LRs are now operational, with around half of those replacing older A320s, contributing approximately $7 million incremental EBIT per hull through fuel and scale efficiencies.

The first QantasLink A220 started flying in March with three of the new aircraft now operating across the network and receiving positive feedback from customers and crew.

QantasLink announced in June the investment in 14 mid-life Q400 turboprops to gradually replace the smaller Q300 and Q200 aircraft, as part of its ongoing commitment to keeping regional Australia connected.

Aircraft manufacturers (including seat suppliers) are continuing to experience supply chain issues, which are resulting in delays to aircraft deliveries for all airlines. Qantas now expects its first A321XLR to arrive in April 2025.

Preparations for the new aircraft have started with pilot training underway and details of the inflight cabin experience finalised. Please see separate media release.

Customer and People

Since September 2023, Qantas has completed more than 120 customer initiatives and service level enhancements from a dedicated engineering team to refresh cabins, the introduction of baggage tracking and route-specific menu changes.

On the back of this investment, customer satisfaction and the Net Promoter Scores across Qantas and Jetstar’s domestic and international services and Loyalty all improved significantly from lows in September 2023. Qantas’ reputation score[7], has also improved over this period, up 12 points to 63 in June 2024, and improved further to 67 in July. The Group expects further improvement as it continues to focus on consistently delivering for customers.

Customers have also benefitted as Group domestic fares were 8 per cent lower than last year and Group international fares were 10 per cent lower, adjusted for inflation, as capacity continues to normalise.

The Group continued to invest heavily in people, including recruitment and training with new aircraft a key driver of new jobs. Up to 2,000 full time roles were added during the year including pilots, engineers, cabin crew and airport staff and 2,300 existing employees progressed internally.

Across the financial year, employee engagement improved, attrition declined and high job applications continued with 150,000 applications received across 4,700 advertised roles.

Sustainability, community and governance

Sustainability remains a key priority for the Group as it takes action towards its 2030 interim target of 25 per cent net emissions reduction (from 2019 levels) and 2050 net zero emissions target.

The Qantas Group has committed significant investments in decarbonisation projects through its Climate Fund, including second round funding for a sustainable aviation fuel (SAF) project in Townsville, $75 million in an international SAF development fund and $20 million in a fund targeting Australian high-integrity nature-based carbon projects.

The Group continues to advocate for the establishment of a domestic SAF industry, which has the potential to generate significant economic benefit for Australia, drive job creation and contribute to national fuel security.

In FY24, Qantas renewed its agreement to purchase SAF for flights out of Heathrow for a third year and doubled the size of its corporate customer SAF program.

The Group continued to spend on community initiatives with a focus on having an impact in Australian communities, including a new 10-year partnership with the Great Barrier Reef Foundation and a major new agreement with the Australian Red Cross. This builds on a number of regional initiatives including providing $50 million in discounts to residents in remote and regional areas and providing another $2 million in grants for regional community groups.

The Qantas Board and management team have been implementing actions in response to recommendations in the Governance Review undertaken to scrutinise decision-making and governance processes of the Board that led to the loss of trust amongst stakeholders. Many actions are already completed or underway.

Outlook

The Group is seeing stable travel demand across the portfolio with positive revenue momentum heading into 1H25.

Group Domestic unit revenue is expected to increase by 2-4 per cent in the first half of the financial year compared to the previous year.

Group International unit revenue is expected to fall 7-10 per cent over the same period as market capacity continues to restore however this rate of decline is expected to slow in FY25. This unit revenue is expected to turn positive in the fourth quarter compared to the prior corresponding period. Net freight revenue in 1H25 is expected to be $20-40 million higher compared to the first half of last year.

Other key assumptions and expectations are summarised below; please see the full Investor Presentation for more detail.

- 1H25 fuel cost at approximately $2.7 billion[8] inclusive of hedging and gross carbon cost of approximately $35 million[9].

- FY25 depreciation and amortisation is expected to be approximately $2 billion.

- FY25 net finance costs are expected to be approximately $270 million.

- Targeting transformation of approximately $400 million in FY25 to offset CPI inclusive of cost and revenue initiatives.

- Net debt expected to be at or below middle of the net debt target range[10].

- The gross impact of Same Job Same Pay in FY25 is approximately $60 million. Looking to be offset through revenue and cost savings.

- Entry into service (EIS) costs to grow approximately $30 million in FY25 in line with acceleration of new fleet deliveries.

- Management remains committed to performance targets[11].

Qantas Group Capacity

| Capacity Guidance[12] (vs prior corresponding period) | 1Q25 | 2Q25 | 1H25 | 2H25 | FY25 | |

| Group Domestic | +1% | +4% | +2% | +2% | +2% | Group Domestic ~104% of pre-COVID capacity for 1H25 |

| Qantas Domestic | (2%) | +1% | (1%) | +3% | +1% | |

| Jetstar Domestic | +7% | +7% | +7% | +1% | +4% | |

| Group International (ex. JSA) | +15% | +17% | +16% | +12% | +14% | Group International (ex. JSA) ~102% of pre-COVID capacity for 1H25 |

| Group International (incl. JSA) | +17% | +19% | +18% | +13% | +16% | |

| Qantas International | +13% | +12% | +12% | +8% | +10% | |

| Jetstar International (ex. JSA)[13] | +21% | +30% | +25% | +22% | +24% | |

| Jetstar Asia (JSA) | +76% | +66% | +70% | +41% | +53% | |

| Total Group | +11% | +13% | +12% | +9% | +10% |

CLICK HERE TO DOWNLOAD PDF OF ASX/MEDIA RELEASE.

[1] Items not included in Underlying Profit Before Tax include impact of the ACCC settlement and increase in provisions for the ground handling outsourcing case.

[2] Percentage of Qantas Domestic and QantasLink and Jetstar domestic flights that departed on time in 4Q24 compared to 2Q24.

[3] Domestic and International Net Promoter Scores 4Q24 compared to 2Q24.

[4] Qantas Domestic Net Promoter Scores 4Q24 compared to 2Q24.

[5] Excluding Jetstar Asia.

[6] Includes Jetstar Australia International long haul, short haul and Trans-Tasman.

[7] RepTrak reputation score.

[8] 1H25 fuel cost based on forecast consumption of ~15.6 million barrels (including SAF); assumes 1H25 market Jet fuel price of approximately A$150 per barrel as at 1 August 2024, excluding into-plane costs and SAF.

[9] Gross cost of SAF and carbon offsets purchased including for compliance, voluntary and customer programs.

[10] Refer to Slide 26 of Investor Presentation for more details.

[11] Airline performance margin targets and Loyalty EBIT target as set at 2023 Investor Day.

[12] ASKs compared to corresponding period in prior year.

[13] Includes Jetstar Australia International long haul, short haul, Trans-Tasman and New Zealand domestic flying.