- Group revenue decrease of three per cent driven by lower international air fares

- Qantas Transformation program and fuel hedging helping protect operating margin

- Qantas Group expecting 1H17 Underlying Profit Before Tax1 of $800m to $850m

The Qantas Group today announced preliminary trading for the first quarter of financial year 2017, with a three per cent decline in revenue due to increased competition on international routes and a subdued domestic demand environment in the first two months of the year.

With continued cost improvement from the Qantas Transformation program and lower fuel prices secured through hedging, the Group expects to deliver a first half underlying profit before tax in the range of $800 million to $850 million. That range would represent the third-best first half result in Qantas’ history.

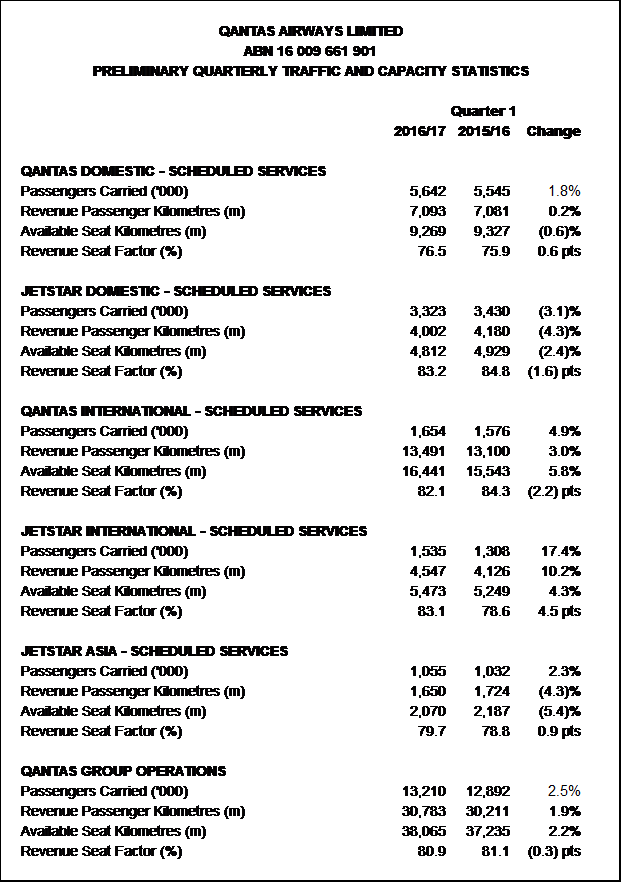

Group revenue for the three month period ending September 30 of $3.98 billion compared to revenue of $4.11 billion in the first quarter of financial year 2016.

Consistent with guidance provided at the Group’s 2016 full-year results, unit revenue (RASK)2 in the quarter was lower than in the prior corresponding period, with a decrease of 5.5 per cent.

Passengers carried rose 2.5 per cent to 13.2 million, driven by Group capacity (Available Seat Kilometres) growth of 2.2 per cent.

Group Domestic Trading

Group Domestic and Jetstar Domestic) unit revenue decreased by 2.9 per cent in the first quarter compared to the prior year period.

The decrease in Group Domestic RASK included a $28 million reduction in resources market revenue in the quarter, primarily in intra-Western Australia and Queensland.

Domestic traffic and unit revenue in July and August were impacted by the overhang of demand softness around the federal election and the absence of one-off events that positively benefited unit revenue in the corresponding period in financial year 2016.

Domestic market conditions in September, outside resources routes, reverted to the more stable environment seen prior to the run-up to the federal election.

Group Domestic capacity reductions reflected the more subdued demand environment at the start of the three-month period, the phasing of school holidays and major events activity.

Group International Trading

Group International (comprising Qantas International, Jetstar International and Jetstar Asia) unit revenue decreased by 6.9 per cent in the quarter with lower fuel prices and higher levels of market capacity growth resulting in more competitive industry-wide pricing.

New Qantas International routes continue to meet expectations though have lowered average international unit revenue during their ramp-up phase.

Qantas International increased capacity by 5.8 per cent, with all growth funded by the increased utilisation of existing Group fleet. Aircraft freed up from the domestic Australia market have been re-deployed for efficient growth, primarily to Asia in response to growing inbound demand from the region.

Jetstar International capacity growth of 4.3 per cent reflected the completion of the transition to a fleet of eleven B787-8 Dreamliner widebody aircraft in the prior financial year.

Qantas Loyalty Trading

Qantas Loyalty saw continued growth in the core Qantas Frequent Flyer (QFF) program, with members growing to 11.5 million as at September 30.

During the quarter, Qantas Frequent Flyer launched a new loyalty partnership with Woolworths, Australia’s largest retailer. The expanded deal provides strong member earn options, a broader category reach, and has returned growth to the retail portfolio of QFF from its commencement in September.

Other new earn partners to join the QFF coalition include Airbnb, Intrepid, Oroton and Deliveroo.

Qantas Loyalty has continued to invest in the growth of its adjacent businesses, including Qantas Cash and Qantas Assure. Qantas Assure’s customer acquisition in its first six months has provided confidence the business will meet its target of capturing a two to three per cent share of the Australian health insurance market.

First Half 2017 Outlook

The Qantas Group expects to report an Underlying Profit Before Tax in the range of $800 million to $850 million for the first six months of financial year 2017.

The expected $800 million to $850 million range compares to an Underlying Profit Before Tax of $921 million in the first half of financial year 2016, and reflects cost improvement from the Qantas Transformation program and lower fuel prices partly offsetting weaker revenue.

Group Domestic unit revenue performance in the second quarter of the financial year is expected to improve compared to the first quarter.

Group International RASK performance in the second quarter is expected to decline at a similar rate as in the first quarter.

At current forward market AUD prices, the Group’s first half fuel cost is expected to be $1.5 billion. That compares to a $1.7 billion fuel cost in the first half of financial year 2016.

Based on a Brent forward market price of A$68 per barrel for the remainder of financial year 2017, the Group’s full year fuel cost is expected to be $3.15 billion, and no worse than $3.2 billion3.

All fuel cost guidance is inclusive of option premium.

Group capacity for the first half of the 2017 financial year is expected to increase by between 1.5 per cent to 2 per cent, revised downwards from previous guidance for growth of between 2 and 3 per cent.

Group Domestic capacity in the first half is expected to decrease by around 1 per cent. Group International capacity is expected to increase by around 3.5 per cent.

The guidance and expectations set out above are subject to no material and unexpected worsening in operating conditions or material unforeseen adverse events.

Buy-Back Update

On 24 August, Qantas announced it would buy-back up to $366 million of shares, subject to approval by shareholders at the AGM on 21 October which was subsequently received. Up to 26 October, the company had completed $141 million of the buy-back, acquiring 44,187,008 shares.

A copy of the latest Form 484 lodged with ASIC shows the total number of shares on issue after cancellation of shares acquired up to 26 October is 1,874,614,006. This represents a 14.6 per cent reduction in shares on issue since 1 July 2015.

Commentary from Qantas Group CEO Alan Joyce

“This first quarter performance has positioned Qantas to deliver another strong first half result in 2017.

“The Group’s reduced cost base, disciplined financial framework, and portfolio strategy give us the foundations to keep performing well even in a more challenging international revenue environment.

“Like most carriers globally, we are seeing international air fares below where they were 12 months ago, but the impact of that is tempered by the competitive advantages we’ve been working hard to fortify including our strong domestic position and diversified Loyalty business.

“Qantas Domestic, Jetstar Domestic and Qantas Loyalty all continue to perform well with high operating margins in a stable market.

“We remain disciplined on cost, continue to manage capacity carefully to match demand, and have secured the benefit of lower fuel prices through our hedging. And at the same time, we will continue to invest in building the Group’s long term competitive advantages, including our brand, customer service and product.”

Recent Developments

- 16 September: Qantas announced a new, daily Melbourne-Narita service, to commence in December 2016, in responses to growing demand and marking the next step in its Asian growth strategy. Post February 2017, Jetstar will withdraw from the route and re-allocate capacity elsewhere on its network.

- 21 September: Qantas released the 2016 Data Book. To access a copy of the 2016 Data Book please visit the Qantas Investor Relations website or click here.

- 30 September: Qantas announced it has extended its debt maturity profile, with the issuance of the following unsecured fixed rate notes:

A$250 million with a semi-annual coupon of 4.40 per cent, maturing in October 2023; and

A$175 million with a semi-annual coupon of 4.75 per cent, maturing in October 2026. - 30 September: Qantas Freight and Australia Post Group announced a five-year extension of their agreement for international air mail. The total value of the contract with the Australia Post Group is in excess of $500 million over five years.

- 4 October: Qantas announced a new partnership enabling frequent flyers to earn points on Airbnb bookings when made through the Qantas website.

- 13 October: Qantas announced it will resume Sydney-Beijing services, with daily flights to begin in January 2017. The new service will allow Qantas to take advantage of the significant growth of the Australia-China travel market.

- 18 October: Qantas opened its new premium international lounge at Brisbane Airport.

- 25 October: Qantas was recognised with a position on the Carbon Disclosure Project ‘Climate A List’ representing the top 9 per cent of global CDP respondents.

- 27 October: Qantas announced its new-look brand and aircraft livery in preparation for the arrival of the Boeing 787-9 Dreamliner in October 2017, in addition to the cabin configuration for the new fleet type.

1 Underlying PBT is a non-statutory measure and is the primary reporting measure used by the chief operating decision-making bodies (being the Chief Executive Officer, Group Management Committee and the Board of Directors) for the purpose of assessing the performance of the Qantas Group.

2 Unit revenue (RASK) is calculated as ticketed passenger revenue per ASK.

3 Worst case total fuel cost as at 31 October 2016. Based on a 2-standard deviation move in Brent forward market prices to US$67/bbl with AUDUSD rate at 0.76, for the remainder of FY17.

Notes

Any adjustments to preliminary statistics will be included in the year to date results next reporting period. Where figures have been rounded, discrepancies may occur between the sum of the components of items, the total and percentage changes which are derived from figures prior to rounding. The number of passengers carried is calculated on the basis of origin/destination (ie. one origin/destination journey represents one passenger regardless of the number of stage lengths undertaken).

Key

(m): Millions

RPKs: The number of paying passengers carried multiplied by the number of kilometres flown ASKs: The number of seats available for sale multiplied by the number of kilometres flown